Washington's AI War: Where Opportunity Hides

The regulatory chaos everyone fears is creating asymmetric opportunity

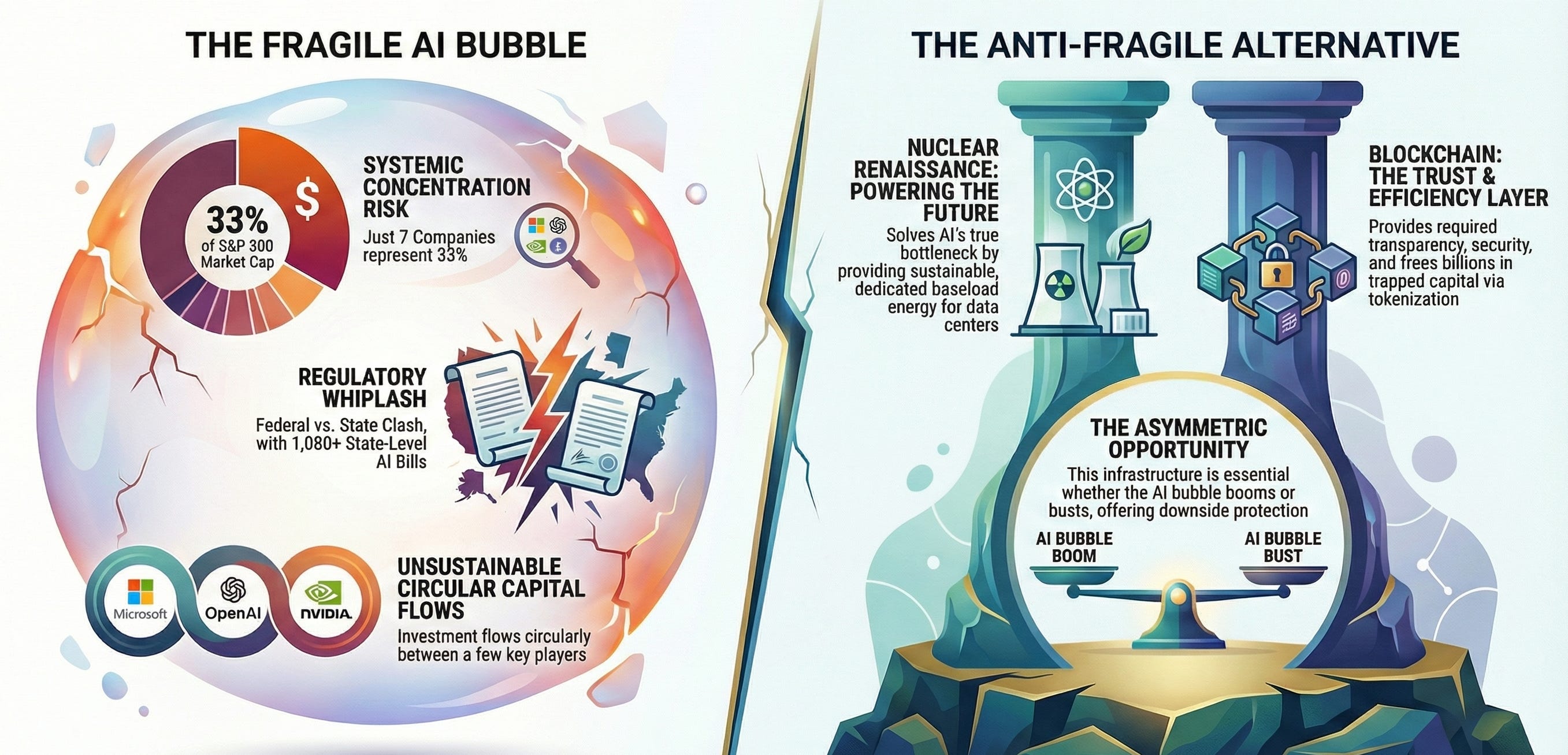

Andreessen Horowitz just published a nine-pillar framework for federal AI legislation. The timing isn’t coincidental. With trillion-dollar valuations straining credibility and circular capital flows propping up concentrated positions, even Silicon Valley’s biggest boosters acknowledge what skeptics have argued: the current market structure is unsustainable.

As a16z themselves concede, pursuing “short-term valuations at the expense of sustainable tools and healthy markets” represents failure, not triumph.

The Regulatory Battlefield

President Trump’s December 11th Executive Order attempts to preempt state AI regulation through a DOJ “AI Litigation Task Force” and conditional federal funding. But executive orders can’t overturn existing law—that requires Congress or courts.

Meanwhile, states aren’t backing down. Over 1,080 AI bills were introduced across all 50 states in 2025; 118 became law. A coalition of 36 state attorneys general is actively opposing federal preemption efforts. Congressional attempts at a ten-year moratorium on state regulation have repeatedly failed.

For investors, this fragmentation is signal, not noise. The companies most exposed to regulatory whiplash are precisely those dependent on circular capital flows: Microsoft → OpenAI → NVIDIA → Oracle → back to NVIDIA. Regulatory disruption anywhere becomes systemic risk everywhere.

The Monopolization Thesis

History shows transformative technologies follow a predictable path: capital-intensive growth funded by speculation, followed by consolidation where winners achieve profitability through market dominance. Amazon, Meta, and Uber all burned capital until reaching monopolistic positions.

The AI sector appears to be following this playbook at hyperspeed. The question isn’t whether AI will transform industries—it will. The question is whether current valuations reflect the timeline to profitability.

Consider the structural constraints: data centers consume massive quantities of freshwater and electricity, with communities absorbing infrastructure costs while benefits accrue to shareholders. AI systems require computational objectives, well-defined parameters, and massive clean datasets. The path to profitability requires either monopolistic pricing power or ubiquitous adoption—both scenarios require time horizons that may exceed current capital structures.

The Anti-Fragile Alternative

The a16z framework emphasizes infrastructure—compute, energy, talent. They’re right about the bottleneck: AI needs physical capacity, not just better algorithms.

Nuclear Renaissance: SMRs solve AI’s actual constraint—sustainable power. While others compete for grid capacity, nuclear provides dedicated baseload. Whether AI booms or busts, the world needs clean, reliable energy.

Blockchain Infrastructure: The framework calls for transparency standards and cyber protection—precisely what cryptographic verification provides. RWA tokenization reduces settlement from T+2 to seconds, eliminating billions in trapped capital. Zero-knowledge proofs enable compliant privacy. These systems run on existing infrastructure, no new data centers required.

Targeted AI Implementation: Specific workstream automation with clear compliance paths and measurable ROI—not trillion-dollar hyperscale bets burdened with regulatory uncertainty.

The Asymmetry

When seven companies represent 33% of S&P 500 market cap and AI spending drives one-third of index valuations, concentration risk is systemic. Deutsche Bank’s reported hedging against its AI data center exposure isn’t bearishness—it’s pattern recognition from an institution that navigated 2008.

Smart capital doesn’t wait for regulatory certainty. It positions when asymmetry emerges.

The anti-fragile portfolio performs regardless of outcome: if AI delivers on promises, nuclear powers it and blockchain handles transaction volume. If valuations correct, energy infrastructure and financial rails remain essential.

The lesson from 2008 wasn’t that bubbles burst—it’s that those who recognized concentration risk early could maintain upside participation while protecting downside. Michael Burry made $100M. John Paulson made $20B. The difference? Position sizing when insurance was cheap.

Smart money isn’t just hedging the bubble. It’s building what comes next.

Alpha Research Group is a blockchain and AI venture fund. The Satoshi Genesis Fund launches in 2026.

Sources

a16z, “A Roadmap for Federal AI Legislation” (December 17, 2025)

Executive Order, “Ensuring a National Policy Framework for Artificial Intelligence” (December 11, 2025)

Congressional Research Service, “Regulating Artificial Intelligence: U.S. and International Approaches” (R48555)

National Conference of State Legislatures, “Artificial Intelligence 2025 Legislation”

Gibson Dunn, “Executive Order Takes Aim at State AI Laws” (December 2025)

| A guest post by

|