The On-Chain Future Has Arrived: From Art to NYSE

From Art to Equities, Every Asset Class Converges on Blockchain Rails

Alpha Research Group | January 2026

The New York Stock Exchange announced yesterday that it’s building a platform for tokenized securities. Not a pilot. Not a research initiative. Production infrastructure for 24/7 trading, instant settlement, stablecoin funding, and multi-chain custody.

When the operator of the world’s largest energy clearing house and credit default swap clearing house describes “on-chain market infrastructure for trading, settlement, custody, and capital formation,” we’re witnessing the end of a debate and the beginning of a buildout.

This piece examines what institutional tokenization means across asset classes—from equities to real estate to digital art—and why the infrastructure layer, not the assets themselves, determines who captures value in the transition.

The Settlement Problem Tokenization Solves

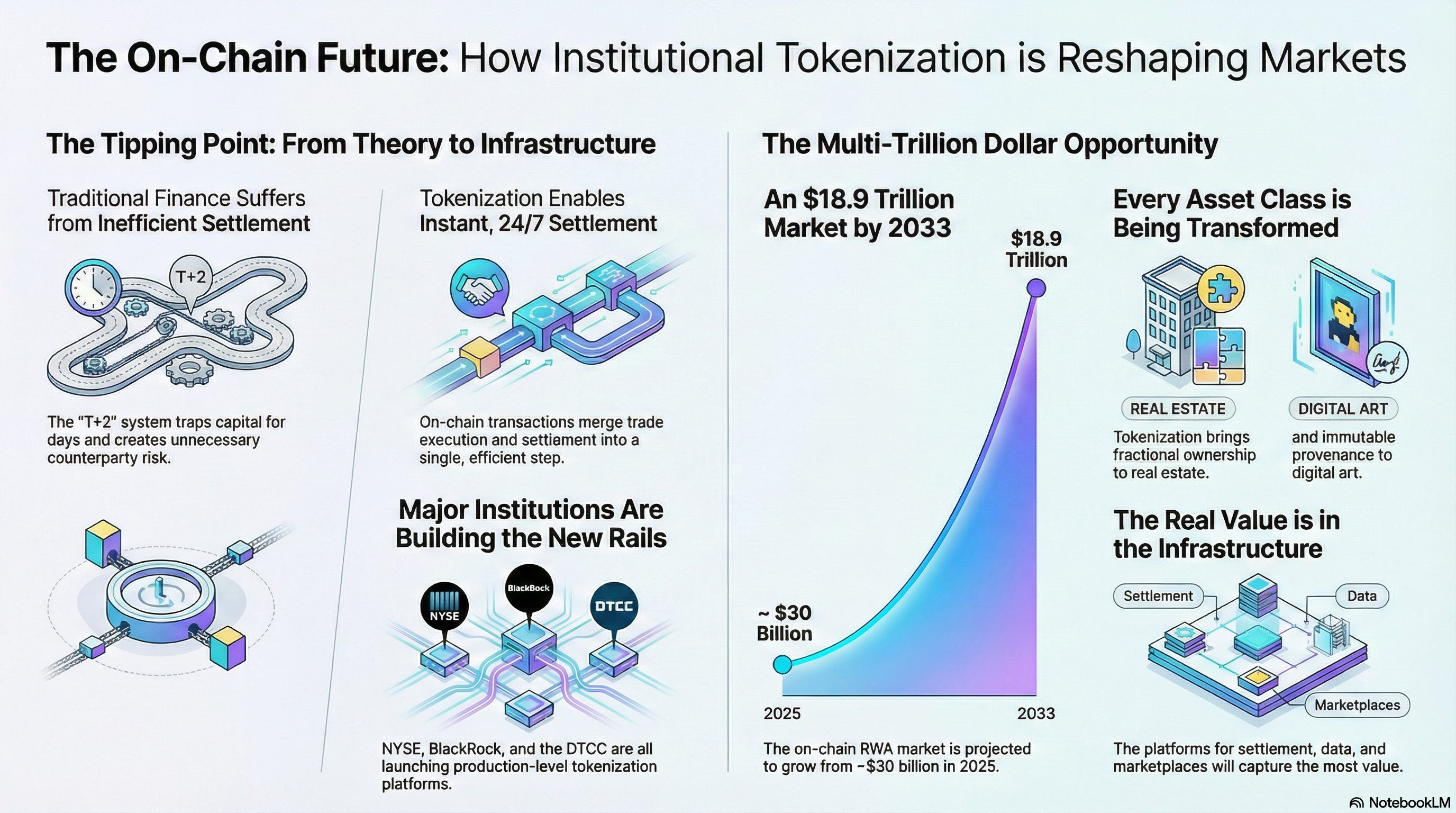

Traditional securities settlement operates on T+2—two business days between trade execution and final settlement. This delay isn’t a feature; it’s a limitation inherited from paper-based systems that required physical certificate transfers. The delay traps capital, creates counterparty risk, and requires complex netting arrangements to manage exposure.

Tokenized settlement eliminates this friction. A trade executes, ownership transfers, and settlement completes in the same transaction. The capital efficiency gains compound across every transaction in the system.

NYSE’s announcement makes the economics explicit: tokenized shares will be fungible with traditionally issued securities, shareholders retain identical dividend and governance rights, and the platform will support multiple blockchains for settlement flexibility. They’re not creating a parallel market—they’re upgrading the rails.

ICE is simultaneously working with BNY and Citi to support tokenized deposits across its clearinghouses. This solves a practical problem: clearing members need to transfer capital and meet margin obligations outside traditional banking hours, across jurisdictions and time zones. Tokenized deposits on blockchain rails operate continuously.

The Depository Trust and Clearing Corporation—which processed $3.7 quadrillion in settlement volume in 2024—has received SEC approval to offer tokenized financial instruments beginning late 2026. The infrastructure buildout is coordinated, not experimental.

The Market Scope: $30 Billion to $18 Trillion

The on-chain RWA market grew from $15.2 billion in December 2024 to over $30 billion by year-end 2025—a 232% increase that understates the acceleration in specific categories.

Tokenized equities grew 27-fold in 2025, from $31.57 million to $858.43 million. Private credit leads overall volume at 61%, with over $18.9 billion in active on-chain credit. Tokenized U.S. Treasuries exceed $8 billion. Real estate tokenization reached $20 billion.

BlackRock’s BUIDL fund—launched on Ethereum with Securitize in March 2024—grew from $40 million to $2.3 billion in assets under management. The fund expanded beyond Ethereum to Aptos, Arbitrum, Avalanche, Optimism, Polygon, and Solana. Larry Fink has openly advocated for tokenization infrastructure, and BlackRock is exploring tokenization of up to $10 trillion in portfolio assets.

McKinsey projects the tokenized RWA market could reach $4 trillion under bullish conditions. Other analyses project $18.9 trillion by 2033. The range reflects uncertainty about adoption curves, not disagreement about direction.

Real Estate: Prediction Markets Meet Data Infrastructure

Housing is the world’s largest asset class—over $50 trillion in the U.S. alone. Yet expressing directional views on housing has historically required property-level complexity, leverage, or long timelines. REITs provide exposure but not precision. Derivatives exist but lack liquidity and accessibility.

This month, Polymarket and Parcl announced a partnership bringing daily housing price indices to prediction markets. Traders can now express views on whether a city’s home price index finishes up or down over defined periods, with transparent settlement against published index data.

The partnership illustrates how tokenization enables market structures that were previously impossible. Parcl provides the data layer—real-time housing indices designed for programmatic access. Polymarket provides the market structure—event contracts that settle against verifiable outcomes. Neither component alone creates the market; the combination does.

Real estate tokenization extends beyond prediction markets. Dubai’s Real Estate Evolution Space Initiative enables blockchain-based fractional ownership with minimum investments of $545. A tokenized villa sale through Prypco sold out in five minutes with 169 investors from 40 countries. The model demonstrates that fractional real estate ownership can attract global liquidity when regulatory frameworks and infrastructure support it.

The Deloitte Center for Financial Services projects $4 trillion in tokenized real estate by 2035. The growth depends on continued regulatory clarity and infrastructure development, but the efficiency gains—reduced transaction costs, faster settlement, fractional accessibility—create persistent pressure toward adoption.

Our early positioning in Parcl as liquidity providers and investors reflected recognition that housing data infrastructure would become essential as tokenized real estate markets developed. The Polymarket partnership validates that thesis, but the broader opportunity is the settlement layer Parcl provides for any market that needs transparent, verifiable housing price data.

Digital Art and Collectibles: Provenance on Immutable Rails

The art market has always been defined by provenance—the documented history of ownership that establishes authenticity and value. Traditional provenance relies on paper records, expert authentication, and institutional reputation. The system works but creates friction: verification takes time, records can be lost or forged, and access to authentication expertise is limited.

Blockchain provides immutable provenance by default. Every transfer is recorded permanently. Ownership history is transparent and verifiable by anyone. Smart contracts can encode royalty structures that persist across secondary sales.

This isn’t hypothetical. The on-chain art market has matured since 2021 from speculative profile pictures to serious collections with institutional recognition. Christie’s, Sotheby’s, and Phillips have conducted significant digital art sales. Museums are acquiring on-chain works. The cultural legitimacy that took traditional art markets centuries to establish is compressing into years.

The more significant development is infrastructure maturation. Early marketplaces were chain-specific and functionally limited. Current platforms operate across multiple chains with sophisticated discovery, curation, and trading tools. Magic Eden now supports Solana, Bitcoin, Ethereum, Base, ApeChain, Arbitrum, Sei, BNB Chain, and Polygon—infrastructure that was built through years of iteration, including launchpad development for Bitcoin Ordinals in 2023 that we contributed to.

Institutional tokenization of traditional equities and assets creates a rising tide for all on-chain markets. As institutions become comfortable with blockchain custody, settlement, and compliance tools, the infrastructure serves digital-native assets as effectively as tokenized traditional assets. The same multi-chain custody solutions that NYSE requires for tokenized equities work for on-chain art collections.

Our collection building since 2021 positioned for exactly this convergence—recognition that institutional infrastructure adoption would validate and support all on-chain asset classes, not just those institutions tokenize directly.

Bitcoin as Platform: Ordinals, Runes, and Native Digital Assets

Bitcoin’s design prioritized security and decentralization over programmability. For years, this meant Bitcoin served as a store of value while other chains hosted more complex applications.

That changed with Ordinals. Casey Rodarmor’s protocol, launched in January 2023, enabled inscribing data directly onto individual satoshis—creating NFT-like artifacts on the most secure blockchain. The innovation wasn’t technical complexity; it was recognizing that Bitcoin’s existing capabilities could support digital artifacts without protocol changes.

The market response was immediate. Over 13 million Ordinal inscriptions were minted within the first year. Magic Eden captured 70% market share in Ordinals trading. Established Ethereum and Solana collections began inscribing Bitcoin versions.

Runes extended the model to fungible tokens. Launching at block 840,000—the April 2024 halving—Runes provided a more efficient token standard than BRC-20, using Bitcoin’s UTXO model rather than inscription-based workarounds. The halving block became the most expensive in Bitcoin history, with users spending $2.4 million in fees to secure early positions.

The significance for institutional tokenization isn’t that memecoins now exist on Bitcoin. It’s that Bitcoin has demonstrated capacity as a platform for tokenized assets, with the security properties institutions require. If Bitcoin can support fungible tokens and digital artifacts, it can support tokenized securities—and Bitcoin’s security model exceeds any other blockchain’s.

Our protocol contributions to Ordinals and first-block Runes positioning reflected thesis conviction that Bitcoin as a platform—not just Bitcoin as an asset—would become institutionally relevant. The NYSE announcement validates that thesis directionally, even though NYSE’s initial implementation will likely use different chains. Institutional comfort with “tokenized assets on blockchain” extends naturally to “tokenized assets on Bitcoin.”

Gaming and Interactive Applications: Ownership Infrastructure

Early blockchain gaming—the “play-to-earn” wave of 2021-2022—failed because it prioritized token economics over gameplay. Players optimized for extraction rather than engagement. Games became jobs rather than entertainment.

The sustainable model is different: games that are genuinely fun, with blockchain enabling ownership of in-game assets without defining the experience. Ownership means players can trade, sell, or transfer items outside the game’s closed ecosystem. It means achievements and assets can persist across games or platforms. It means the value players create through gameplay accrues to them rather than exclusively to developers.

Layer 2 scaling made this model viable. Arbitrum, Optimism, and similar solutions reduced transaction costs enough for high-frequency game interactions. A player buying a sword or completing a quest can happen on-chain without fees destroying the economics.

Proof of Play and similar projects on Arbitrum represent this model—games built for engagement, with blockchain infrastructure enabling ownership and interoperability without forcing players to think about blockchain at all.

Institutional tokenization accelerates gaming infrastructure development through adjacent effects. As institutions build custody, compliance, and trading infrastructure for tokenized securities, that infrastructure becomes available for gaming assets. A custodian that can hold tokenized equities can hold in-game items. A trading venue that supports tokenized real estate can support game asset markets.

The convergence isn’t immediate, but the infrastructure is shared. Our early GameFi positioning anticipated this convergence—recognition that institutional infrastructure development benefits all on-chain asset categories through capability spillover.

Funding Innovation: DeFi Rails for Venture Capital

Traditional venture capital operates on structures developed decades ago: equity purchases, dilution, long hold periods, illiquidity until exit events. The model works but creates friction for both founders and investors.

Founders accept dilution with each funding round, eventually owning small percentages of companies they built. Investors accept illiquidity, with capital locked for 7-10 years without meaningful return potential until IPO or acquisition.

DeFi infrastructure enables different models. Principal-Preserved Protocol Funding (P3F)—a mechanism we developed—preserves investor principal through stablecoin deposits on regulated platforms while generating operational funding through yield. Multi-signature governance ensures appropriate controls. Founders receive funding without traditional dilution. Investors maintain capital protection while gaining portfolio exposure.

This isn’t theoretical—it’s operational, using stablecoins, yield protocols, and multi-sig governance that now provide institutional reliability. The mechanism would have been impossible five years ago; infrastructure maturation made it viable.

Institutional tokenization extends the possibilities. If equities can be tokenized with instant settlement, so can venture interests. If stablecoins serve as funding mechanisms for NYSE trading, they can serve as funding mechanisms for venture portfolios. The regulatory frameworks and infrastructure being built for institutional asset tokenization apply to venture structures.

The stablecoin market itself—which grew from $216 billion to $306 billion in 2025—reflects institutional adoption of blockchain-native settlement assets. As regulatory frameworks mature (the SEC and CFTC joint statement on 24/7 capital markets, Europe’s MiCA implementation), stablecoin infrastructure becomes increasingly institutional rather than crypto-native.

Privacy and Compliance: The Infrastructure Requirements

Institutional tokenization requires solving a tension: blockchain’s transparency is a feature for verification but a problem for confidentiality. Institutional investors need privacy for positions and trading activity. Regulatory compliance needs visibility for oversight and enforcement.

Zero-knowledge proofs address this tension by proving transaction validity without exposing underlying data. A compliance system can verify that a trade meets regulatory requirements without knowing the parties’ identities or the specific amounts involved until appropriate disclosure is required.

This isn’t speculative technology. Zero-knowledge systems are production-ready and increasingly integrated into institutional infrastructure. The same capabilities that enable privacy-preserving compliance for crypto-native applications enable it for tokenized securities.

Our research on blockchain privacy and zero-knowledge implementations examined how these systems preserve both privacy and regulatory compliance—recognizing that institutional adoption requires solving this tension, not ignoring it.

The Strategic Reserve and Sovereign Adoption

The U.S. Strategic Bitcoin Reserve—established by executive order in March 2025—represents sovereign recognition of Bitcoin as a strategic asset. The reserve, initially funded from seized Bitcoin holdings, established a framework for federal cryptocurrency accumulation.

Senator Lummis’s proposal for Treasury to acquire 200,000 BTC annually over five years would create federal holdings of one million Bitcoin—approximately 5% of total supply. The funding mechanism—profits from Federal Reserve bank deposits and gold holdings—would make accumulation budget-neutral.

We published analysis making the case for strategic Bitcoin reserves before the announcement, examining how sovereign reserve logic that applies to gold and foreign currencies applies to Bitcoin’s properties as digital scarcity.

The strategic reserve creates downstream effects for tokenization. Federal legitimization of cryptocurrency as a reserve asset accelerates institutional comfort with all blockchain-based assets. A sovereign that holds Bitcoin has implicitly endorsed the security and durability of blockchain infrastructure generally.

Multiple U.S. states are now considering their own strategic Bitcoin reserve integrations. The Czech National Bank governor has expressed interest. El Salvador continues expanding its holdings. Sovereign adoption is becoming normalized rather than exceptional.

Forward Positioning: Where Infrastructure Captures Value

Institutional tokenization creates value at the infrastructure layer, not primarily at the asset layer. NYSE isn’t tokenizing specific equities—it’s building infrastructure that tokenizes all equities. BlackRock isn’t tokenizing individual Treasury bills—it’s building infrastructure that tokenizes Treasury exposure at scale.

The pattern holds across asset classes:

Settlement infrastructure captures value from every transaction, regardless of which specific assets trade. Chainlink’s CCIP, multi-chain custody solutions, and compliance tooling serve institutional requirements across asset types.

Data infrastructure captures value from any market that needs verifiable, programmatic information. Parcl’s housing indices serve prediction markets today; they can serve tokenized real estate settlement, mortgage verification, or any application requiring transparent housing data.

Marketplace infrastructure captures value from trading activity across asset categories. The launchpad, trading, and custody tools built for Ordinals and NFTs serve tokenized gaming assets, digital art, and eventually tokenized traditional assets as markets converge.

Funding infrastructure captures value from capital flows that move to blockchain rails. As stablecoin volume grows and regulatory frameworks mature, funding mechanisms that leverage DeFi infrastructure serve both crypto-native and traditional applications.

Our positioning since 2021 has consistently targeted infrastructure rather than specific assets—protocol contributions, launchpad development, data platform investment, funding mechanism innovation. Institutional tokenization validates this approach by demonstrating that infrastructure built for crypto-native applications serves institutional requirements as those requirements move on-chain.

Conclusion: Infrastructure Meets Institutional Capital

The NYSE announcement represents a phase transition, not a new direction. Tokenization has been developing for years across every asset class—art, real estate, gaming assets, Bitcoin-native tokens, private credit, Treasuries. What’s changing is the scale and legitimacy of institutional participation.

When ICE builds on-chain clearing infrastructure, when BlackRock manages $2.3 billion in tokenized Treasury exposure, when the DTCC receives approval for tokenized instruments, the infrastructure requirements become clear: multi-chain support, institutional custody, regulatory compliance, efficient settlement.

Early positioning in tokenization infrastructure—data layers, marketplaces, protocols, funding mechanisms—captures value as institutional capital enters on-chain markets. The specific assets matter less than the rails they travel on.

We’ve been building this infrastructure since 2021: protocol contributions to Bitcoin Ordinals, launchpad development for Magic Eden, liquidity provision for Parcl, first-block Runes positioning, GameFi infrastructure backing, DeFi funding innovation. Each position targeted infrastructure that serves multiple asset classes and use cases rather than exposure to specific tokens or projects.

The NYSE announcement is validation, not destination. Institutional tokenization is a multi-decade infrastructure buildout, not a single product launch. The positions that capture value are those that serve institutional requirements as those requirements move on-chain.

Infrastructure built for crypto-native applications serves institutional applications when institutions arrive. They’re arriving.