The Founder Problem: Crypto's Equities Gap and the Ten-Year Fuse

The Quantum Deadline, and Why Satoshi, CZ, and Vitalik Can't Touch Their Own Wealth

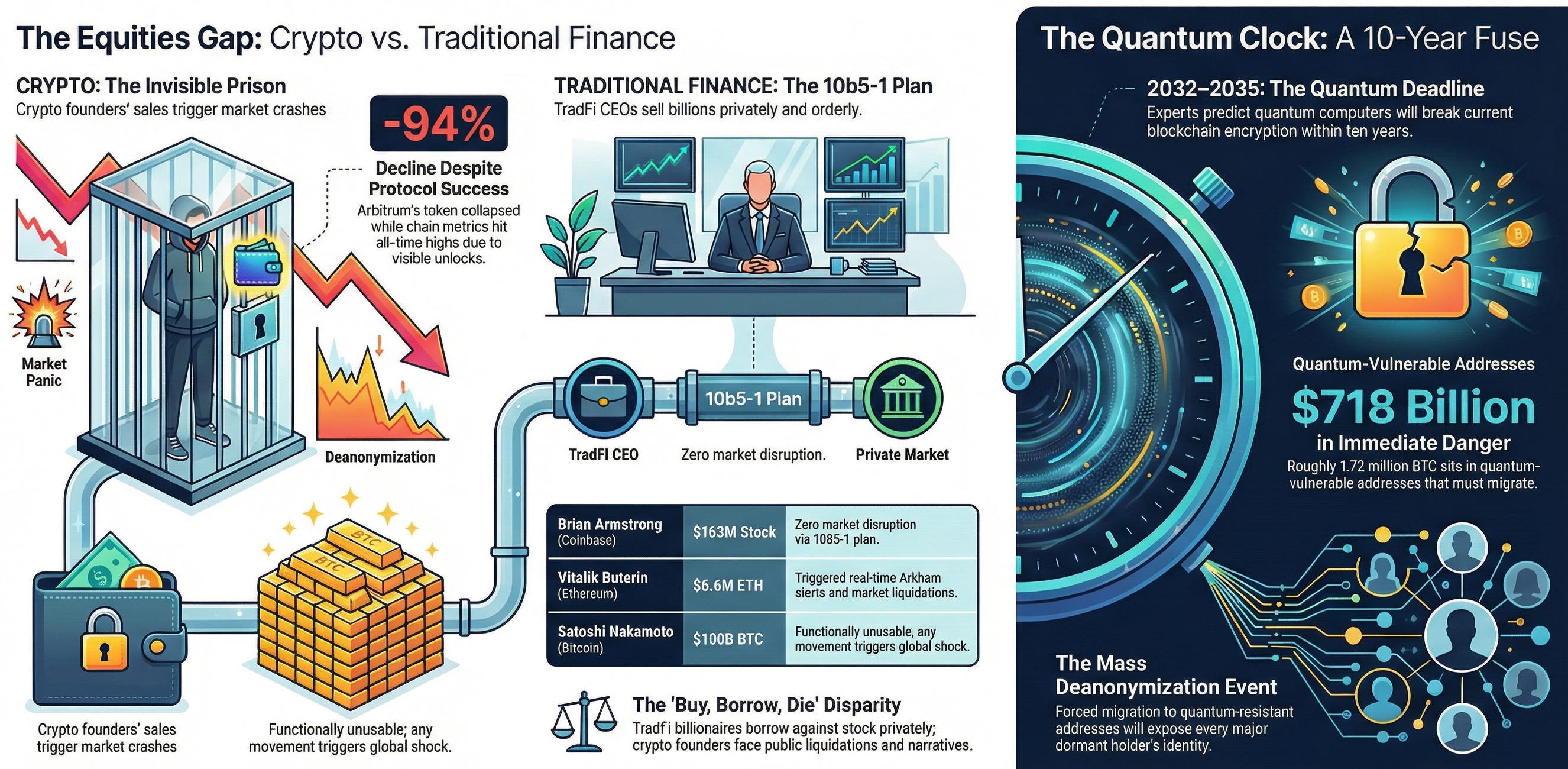

There is a $718 billion problem sitting on the blockchain, and it has a ten-year fuse.

Every major cryptocurrency founder, early miner, and protocol team in the world shares the same invisible prison: they cannot sell, they cannot move, they cannot borrow against their holdings, and they cannot access DeFi yield — all because the transparent, immutable ledger that made them wealthy is the same system that makes their wealth functionally unusable.

Meanwhile, every traditional finance billionaire in America — Elon Musk, Larry Ellison, Jeff Bezos, Mark Zuckerberg — borrows against their stock, rakes yield, pays taxes privately through normal channels, and never triggers a market event. They don’t sell. They don’t need to. The infrastructure exists to let them access their wealth without destroying it.

We call this disparity The Equities Gap — the structural absence, in crypto, of the private wealth management infrastructure that traditional equity holders have used for decades. It is the single largest unsolved problem in digital assets, it is worsening every cycle, and the quantum computing timeline just turned it from a chronic inconvenience into an existential emergency.

I. The Founder Problem: Wealth You Cannot Touch

Satoshi Nakamoto holds approximately 1.1 million Bitcoin — worth over $100 billion at current prices. That fortune has never moved. Not a single satoshi. Not because Satoshi doesn’t want to access that wealth, but because the mechanics of doing so are effectively impossible.

The moment Satoshi moves a coin, several things happen simultaneously. Chain analysis firms — Chainalysis, Elliptic, Arkham — flag the transaction within seconds. Every major financial news outlet runs the story within minutes. Markets react violently, because Satoshi moving coins is interpreted as either selling pressure or an existential signal about Bitcoin’s future. Regulatory agencies across dozens of jurisdictions begin tracing the movement. And the pseudonymous identity that has protected Satoshi for over sixteen years begins to unravel, because movement creates patterns, and patterns create identification.

This is not unique to Satoshi. It is the structural condition of every significant holder in cryptocurrency — and it extends far beyond the legendary early wallets.

The Roll Call

Consider the most prominent names in the industry and the invisible prison each one occupies:

Satoshi Nakamoto (Bitcoin). The creator of Bitcoin holds approximately 1.1 million BTC — over $100 billion — and has never moved a single satoshi. Satoshi faces the most extreme version of the Equities Gap: any movement from those wallets triggers a global news event, a market shock, and a chain of identity analysis that would unravel sixteen years of pseudonymity. Satoshi cannot fund a foundation, pay a legal bill, donate to charity, or buy groceries using the largest single fortune in crypto. Every other founder on this list at least has the option of selling publicly and absorbing the damage. Satoshi doesn’t even have that.

Changpeng Zhao (Binance). CZ built the world’s largest cryptocurrency exchange, holds an estimated 90% stake in the company, and has publicly confirmed that BNB comprises roughly 98% of his personal crypto portfolio — approximately 89 million tokens. Forbes estimates his net worth between $65 billion and $88 billion depending on the day, placing him among the twenty-five wealthiest people on earth. Yet CZ cannot meaningfully touch that wealth. If any wallet linked to him moves a material amount of BNB, the market moves with it — not because of fundamentals, but because of the signal. Post-DOJ settlement and presidential pardon, CZ sits on one of the largest single-asset concentrations in financial history with effectively zero private liquidity access. He has publicly endorsed a HODL strategy, but “holding” is not a strategy when it’s the only option. CZ doesn’t hold because he wants to. He holds because the infrastructure to do anything else doesn’t exist.

Vitalik Buterin (Ethereum). The Ethereum co-founder’s situation is examined in detail in Section III, but the summary is stark: Buterin holds approximately 227,000 ETH, has watched his holdings decline from over $1.6 billion at the 2021 peak, and is currently selling into a down market to fund the Ethereum Foundation and his Kanro biotech charity — realizing cash at the worst possible prices because no privacy-preserving alternative exists.

Hayden Adams (Uniswap). The creator of the largest decentralized exchange faces the same trap from the governance side. When the Uniswap DeFi Education Fund sold $10 million in UNI immediately after receiving a treasury grant — a grant that had promised deployment over four to five years — the community erupted. Charlie Watkins of Curve Finance called the grantees “opaque lobbying organisations.” DeFi Watch founder Chris Blec demanded transparency about the fund’s origins, governance capture by VCs (Andreessen Horowitz delegates provided the margin of victory), and conflicts of interest. Any operational transaction touching Uniswap’s treasury or associated wallets generates the same firestorm. Adams built the most important piece of DeFi infrastructure in existence, and his protocol cannot fund basic operations without a governance crisis.

These are not isolated cases. They are the structural condition of the industry.

The ICO and TGE Trap

The Equities Gap doesn’t only affect legendary founders. It affects every core team, every protocol treasury, and every organization that emerged from an ICO or Token Generation Event.

Consider the pattern. A team spends years building a protocol. They launch a token — through an ICO, a fair launch, an airdrop, a TGE. The token vests over time. The team needs to pay salaries, fund development, cover legal costs, rent office space, and live their lives. The only liquid asset many of these teams hold is their own token.

And the moment they sell any of it — for any reason — the market punishes them.

The Ethereum Foundation has become the most visible example. The Foundation has sold ETH consistently to fund operations — averaging a sale roughly every eleven days throughout 2024, totaling $9.67 million. In 2025, they sold 36,000 ETH through CoW Swap. In September 2025, they moved 10,000 ETH ($42.7 million) to Kraken to cover research, grants, and donations. Every single sale triggered community backlash. Crypto analyst Eric Conner captured the sentiment: “The EF uses the chain, actually our number one use case is dumping ETH. Actually insane.” DCinvestor, one of Ethereum’s most vocal advocates, went further — saying Trump-backed World Liberty Financial was “more aligned with the success of Ethereum-based DeFi than the Ethereum Foundation is.”

This is a foundation selling modest amounts to pay researchers and fund grants. Operational expenses. Payroll. The most basic obligations any organization has. And the market response is outrage.

Arbitrum (Offchain Labs) faces the same trap on a structural level. After the ARB airdrop in March 2023, the token traded around $1.20-$1.50. Then team and investor unlock cliffs began hitting in March 2024 — roughly 92.63 million ARB per month, nearly 1% of max supply. The token didn’t collapse in a single candle. It bled slowly, month after month, from its January 2024 high of $2.40 to an all-time low below $0.13 in early February 2026 — a decline exceeding 94% — while the underlying chain posted all-time highs in TVL, stablecoin supply, bridge inflows, and daily active users. Arbitrum the product is thriving. ARB the token is in a death spiral driven entirely by the visible, trackable, unavoidable reality that vesting tokens must eventually be sold.

These are not cases of founders getting rich and running. These are teams and foundations trying to fund operations — payroll, legal, development, grants — using the only liquid asset available to them. And in every case, the transparent on-chain nature of the transaction transforms a routine operational expense into a market-moving, narrative-destroying event.

No Fortune 500 CFO has ever faced a stock crash because the company sold shares to fund quarterly operations through a registered offering. The mechanism exists — secondary offerings, ATM programs, structured sales — and the market absorbs them without panic because the infrastructure handles the transaction privately and orderly.

Crypto has no equivalent. That is the Equities Gap.

OTC Is Not an Exit

The natural counterargument is OTC — over-the-counter sales through institutional desks. In theory, OTC provides a private channel for large block sales without market impact.

In practice, OTC leaks signal like a sieve.

The major OTC desks and clearing houses — Cumberland, Circle Trade, Galaxy Digital, Genesis — require counterparty discovery, price negotiation, and settlement that telegraphs into the market. The desk needs to hedge. The counterparty needs to source liquidity. Market makers who service these desks adjust their positioning the moment a large block is being shopped. The result is that OTC “private” sales routinely front-run themselves — price moves before settlement because the market infrastructure required to execute the trade broadcasts its existence.

Wallet movements to known OTC staging addresses are tracked by the same analytics firms monitoring the public chain. A large holder moving coins to a known OTC deposit address is functionally equivalent to announcing a sale. Arkham Intelligence has made a business model out of exactly this kind of deanonymization and movement tracking. When the Ethereum Foundation moved 10,000 ETH to Kraken in September 2025, Arkham flagged it within minutes. The backlash started before the first ETH was sold.

There is no quiet exit in crypto. There are only loud exits and slightly-less-loud exits. And every one of them costs the seller — and their token holders — value.

II. The Quantum Clock: Ten Years to Move or Lose Everything

Everything above has been true since Bitcoin’s inception. Founders and whales have lived with the Equities Gap for years. What transforms this from a chronic structural problem into an existential emergency is the quantum computing timeline.

Current estimates converge on a window between 2032 and 2035 for a Cryptographically Relevant Quantum Computer (CRQC) capable of running Shor’s algorithm against the ECDSA signatures that secure Bitcoin, Ethereum, and virtually every major blockchain. This is not speculation from crypto Twitter. This is the position of the institutions that define cryptographic standards for the free world.

NIST has directed all U.S. federal agencies to complete migration to post-quantum cryptography by 2035. The Federal Reserve published a formal paper in 2025 examining the “Harvest Now, Decrypt Later” threat to blockchain systems. Peer-reviewed research in ScienceDirect concluded that by 2035, quantum computers are “more likely than not” to be capable of breaking RSA-2048 — the security benchmark comparable to Bitcoin’s elliptic curve cryptography. Recent estimates put a 17% to 34% probability of a CRQC existing by 2034, increasing to 79% by 2044.

The specific vulnerability: Bitcoin’s early Pay-to-Public-Key (P2PK) addresses expose public keys directly on the blockchain. A quantum computer running Shor’s algorithm can derive the private key from the public key. According to Chainalysis and Project Eleven, approximately $718 billion worth of Bitcoin sits in quantum-vulnerable addresses today. That represents roughly 1.72 million BTC — including Satoshi’s estimated holdings — where the public keys are already harvested and waiting.

The “Harvest Now, Decrypt Later” strategy is not theoretical. Nation-state adversaries are already collecting exposed public keys from every major blockchain. When a CRQC arrives, every wallet whose public key was ever exposed becomes immediately vulnerable. The keys are already harvested. The decryption is just waiting for the hardware.

This means every dormant wallet must migrate to quantum-resistant addresses, or the funds will be stolen.

There is no opt-out. If you hold significant crypto in pre-quantum address formats and you do not move to post-quantum safe custody before a CRQC exists, your wealth is gone.

This creates the largest forced movement event in cryptocurrency history. Millions of wallets — including Satoshi’s, including CZ’s dormant reserves, including every early miner, including every significant dormant position — must move. Bitcoin’s protocol will need to implement post-quantum signature schemes. Ethereum faces the same migration.

And here is the part nobody is discussing honestly: this forced migration will necessarily expose the identity of every early holder who has relied on dormancy as their privacy model.

When 1.72 million BTC in P2PK addresses suddenly begins migrating, chain analysis firms will map every movement. Patterns will emerge. Wallets that were previously dark will become active — and active wallets leave traces. The quantum migration is not just a technical upgrade. It is a mass deanonymization event.

For Satoshi, for CZ, for Buterin, for every whale who has relied on “don’t move, don’t get found” as their security model — the quantum clock is a countdown to forced exposure.

Unless there is a privacy layer to migrate through.

III. The Vitalik Validator: Same Behavior, Different Infrastructure

You don’t need to theorize about what the Equities Gap looks like in practice. Ethereum’s co-founder is demonstrating it in real time — and the comparison to traditional finance couldn’t be more instructive.

As of February 5, 2026, Vitalik Buterin (Ethereum) has sold 2,961 ETH ($6.6 million) over three days at an average price of $2,228. Ethereum is trading around $2,080 — down nearly 30% on the week. Over $210 million in long ETH positions have been liquidated in the past 24 hours. DeFi TVL has fallen below $100 billion for the first time in nine months. A single short seller on Hyperliquid made $102.7 million betting against ETH during this collapse.

And the co-founder of the network is market-selling into it.

Buterin is not doing anything wrong. He is doing exactly what every public company executive does — selling equity to fund operations and philanthropy. His stated reasons — funding the Ethereum Foundation during “mild austerity” and supporting his Kanro biotech charity — are legitimate, disclosed, and consistent with years of transparent behavior. He publicly announced the allocation of 16,384 ETH to support long-term open-source and infrastructure initiatives. This is responsible, deliberate stewardship.

The problem is not Buterin’s behavior. The problem is the infrastructure gap that makes identical behavior produce catastrophically different outcomes.

The Armstrong Contrast

Consider Brian Armstrong (Coinbase). Armstrong operates in both worlds — crypto founder and publicly traded company CEO. Through a pre-established Rule 10b5-1 trading plan adopted in August 2024, Armstrong has executed regular, structured sales of Coinbase stock: $99.9 million in November 2024. $19.1 million later that same month. $8.52 million in December. $6.5 million in January 2025. $6.88 million in February. $1.98 million in March. $2.68 million in April. $163 million in June 2025. Hundreds of millions of dollars in founder stock sales over eight months.

The market response to each of these sales was: nothing.

No panic. No narrative collapse. No accusations of abandoning ship. No cascading liquidations. No short sellers engineering attacks around the disclosed positions. Armstrong’s sales appeared in SEC filings that analysts reviewed and institutional investors absorbed as routine. COIN’s stock price was driven by fundamentals, not by founder transaction surveillance.

Armstrong sold more value in a single June transaction ($163 million) than Buterin has sold in years of combined ETH disposals. The difference is entirely infrastructure. Armstrong has a 10b5-1 plan, an SEC filing process, a regulated framework that operates with appropriate privacy at the transaction level. The market knows he sells. The market doesn’t panic because the mechanism is familiar, orderly, and managed.

Now look at Buterin. When he sells $6.6 million — a fraction of what Armstrong moves in a routine quarter — Arkham flags it in real-time. Lookonchain broadcasts it to millions. Crypto Twitter amplifies it as “the founder is dumping.” Short sellers on Hyperliquid use the information to build positions. Cascading liquidations follow. The market processes identical behavior — a founder selling equity to fund operations — as a crisis, because the infrastructure broadcasts the transaction as one.

The absurdity compounds when you examine Buterin’s own wallet. Arkham data shows Buterin already holds approximately 2,928 aETHWETH positions on Aave V3, worth roughly $6.9 million. He already uses DeFi lending. He already understands collateralized borrowing. He has the technical infrastructure to deposit ETH, borrow stablecoins at 30-40% LTV, fund his foundation and charity obligations, and never sell a single token.

Compare this to what any TradFi founder would do. Larry Ellison (Oracle) doesn’t sell stock when he needs cash for a foundation. He borrows against it at 3%, takes a tax deduction on the donation, and his Oracle position continues compounding. The market never sees a sell order. The stock price doesn’t move. Armstrong doesn’t need to borrow — his 10b5-1 plan handles the sales mechanically and the market absorbs them without disruption.

But even borrowing carries risk in crypto without privacy. A large, publicly visible Aave position on a founder’s known wallet becomes a target for short sellers who can calculate exact liquidation prices and engineer cascades. The DeFi tools exist. The privacy to use them safely does not.

Buterin’s situation validates the thesis perfectly — not because he is doing anything wrong, but because he is doing everything right and the outcome is still catastrophic. Even the most sophisticated actors in crypto, with direct access to the protocols they helped create, are forced into value-destructive outcomes because the Equities Gap has never been closed.

When Tim Cook (Apple) executes a pre-disclosed stock sale, it appears in an SEC filing that almost nobody reads. When Buterin sells, Arkham flags it in real-time, CT amplifies it into a narrative event, and cascading liquidations follow. The behavior is identical. The infrastructure gap makes the outcome catastrophic.

IV. The Equities Gap: Buy, Borrow, Die — For Everyone But Crypto

In traditional finance, there is a well-documented wealth management strategy so ubiquitous among the ultra-wealthy that it has its own academic name: Buy, Borrow, Die.

Buy appreciating assets — stocks, real estate, operating businesses. Borrow against those assets using Securities-Backed Lines of Credit (SBLOCs) at rates between 2-5%. Use the borrowed funds for living expenses, investments, philanthropy — without triggering a taxable event. When you die, your heirs receive the assets with a “stepped-up basis” that eliminates all accumulated capital gains tax liability.

This is not a fringe strategy. It is the foundation of American wealth preservation.

Larry Ellison (Oracle) has pledged over $4 billion in Oracle shares as collateral. Elon Musk (Tesla, SpaceX) used Tesla stock to back major acquisitions. Goldman Sachs’ securities-based lending division manages over $175 billion in such loans. JP Morgan, Morgan Stanley, and every major private bank offers 70-90% LTV ratios against diversified portfolios. The Yale Budget Lab documented the scale: more than $175 billion in securities-backed loans outstanding as of 2023, overwhelmingly concentrated among the wealthiest households.

The billionaire borrows at 3%. Their assets appreciate at 8-12%. The spread compounds their wealth. Interest payments are often tax-deductible. The underlying assets never trigger capital gains. And the transactions — the borrowing, the spending, the wealth management decisions — are private. Between the founder, their banker, and the IRS.

Beyond SBLOCs, TradFi founders access an entire ecosystem of private wealth management tools: Special Purpose Vehicles (SPVs), irrevocable trusts, family offices, variable prepaid forward contracts, exchange funds for diversification without realization, and structured philanthropy vehicles. Every one of these tools operates through private channels with regulatory compliance at the appropriate touchpoints.

Crypto founders from every generation of the industry — from Satoshi’s dormant millions to CZ’s frozen BNB empire to Buterin’s operational funding crisis — have access to none of this in a practical sense.

Yes, DeFi lending protocols exist. Yes, you can deposit ETH into Aave and borrow USDC. But every step is public. Your deposit is visible. Your borrow is visible. Your LTV ratio is calculable by anyone. Your liquidation price is known. Short sellers target known whale positions. And if you’re a founder or a foundation, every interaction with a lending protocol generates headlines, speculation, and market impact.

The result is a two-tier system that penalizes the very people who built the industry:

TradFi founders manage their wealth privately, efficiently, and compliantly — accessing liquidity without market disruption, paying taxes through normal channels, and maintaining security through obscurity. Brian Armstrong (Coinbase) can sell $163 million in COIN through a 10b5-1 plan and the market doesn’t flinch. Larry Ellison (Oracle) can borrow $4 billion against his shares and nobody outside his banker’s office knows about it.

Crypto founders are forced to either sit on frozen wealth indefinitely, sell publicly at the worst possible times for even the most basic operational needs, or route through opaque offshore structures that create genuine compliance risk. Vitalik Buterin (Ethereum) sells $6.6 million and triggers cascading liquidations. CZ (Binance) sits on tens of billions in BNB that cannot move without moving the market. Hayden Adams (Uniswap) cannot fund protocol operations without a governance revolt. The Arbitrum (Offchain Labs) Foundation watches its token bleed 94% while its chain posts all-time highs in every operational metric.

When the Ethereum Foundation sells 100 ETH — roughly $230,000, a rounding error for any serious organization — the community erupts. When Armstrong sells $99.9 million in Coinbase stock through a pre-arranged plan, it appears in an SEC filing that institutional analysts note and nobody else reads.

No tech CEO in traditional finance faces this. Tim Cook (Apple) doesn’t trigger a stock crash when the company executes a planned share offering to fund R&D. The mechanism exists, it operates with appropriate privacy at the transaction level, and the market absorbs it as routine.

The Equities Gap is not a theoretical inequality. It is a measurable, daily cost borne by every significant crypto holder, every protocol team, and every foundation — and it is driving talent and capital out of the ecosystem.

V. The Regulatory Frame: Legal, Clean, Compliant

The natural objection to privacy-preserving crypto infrastructure is regulatory: doesn’t privacy enable evasion?

No. Privacy enables equality. Evasion is a choice made by individuals, and it exists in every financial system — transparent or private. The question is not whether privacy exists, but whether privacy operates within a compliant framework.

Consider the irony: the current transparent system creates more compliance chaos than privacy would. When Buterin sells ETH publicly, cascading liquidations begin before anyone has assessed the tax implications. When the Ethereum Foundation moves coins to Kraken, front-running starts before settlement. When a founder interacts with Aave, their position becomes a short-selling target. Transparency doesn’t create compliance — it creates chaos, front-running, and unwarranted market punishment for routine financial activity.

Meanwhile, Brian Armstrong (Coinbase) sells hundreds of millions in COIN stock through established TradFi mechanisms — pre-arranged plans, SEC filings, private execution — and the market absorbs it as routine. Legal. Clean. Compliant. Private at the transaction level.

Soulbound’s model is deliberately built on the most familiar and universally accepted compliance architecture in finance: KYC at deposit, privacy at transaction, tax compliance at off-ramp. This is the same framework Armstrong operates under. It is the same framework every TradFi billionaire operates under. It is, in fact, how cash works.

You identify yourself at the ATM or bank window. You withdraw money. What you do with that cash — what you buy, who you pay, how you spend — is private. The bank knows you withdrew $500. The coffee shop doesn’t know your net worth. When you earn income, you report it and pay taxes in your jurisdiction. The system trusts the compliance framework at entry and exit, not surveillance of every intermediate transaction.

Soulbound applies this model to crypto wealth management:

At deposit: Full KYC/AML compliance. Identity verified. Source of funds confirmed. The holder enters the system through a regulated gateway, establishing their tax jurisdiction and reporting obligations. This is the ATM. You identify yourself here.

At transaction: Movement, lending, borrowing, yield generation, and payments occur through privacy-preserving infrastructure. The holder can collateralize positions, access DeFi yield, borrow stablecoins, and transact — without every movement being broadcast on a public ledger for chain analysis firms, short sellers, and the entire market to front-run.

At off-ramp: When the holder exits back to fiat or moves to a public chain, tax obligations are settled in their jurisdiction through the same compliant framework. The off-ramp is the second compliance touchpoint — just like depositing cash back into a bank account or reporting income on a tax return. You deal with your taxes where you live, through established channels, the same way every other asset class works.

This framework does not evade anything. It provides the same transaction-level privacy that every cash transaction, every private banking relationship, every 10b5-1 plan, and every stock lending arrangement in traditional finance already provides — while maintaining the identity verification and tax compliance that regulators require.

Compliant privacy creates orderly markets. Holders can access their wealth without destroying value. Taxes are collected at the jurisdictionally appropriate touchpoints. Regulators can audit through the KYC framework without requiring real-time surveillance of every transaction. And the market is protected from the artificial volatility created by public founder movements and vesting unlocks.

Every billionaire in TradFi manages their wealth this way. Armstrong does it at Coinbase through 10b5-1 plans. Ellison does it at Oracle through SBLOCs. Musk does it at Tesla through structured borrowing. Legal. Clean. Compliant. Private at the transaction level.

Satoshi, CZ, Buterin, Adams, and every crypto builder who ever launched a token deserve the same option.

The Convergence

The Founder Problem, the Quantum Clock, and the Equities Gap are not three separate issues. They are one issue viewed from three angles, and they converge on a single requirement: privacy-preserving payment and wealth management infrastructure that operates alongside the base layer, with full regulatory compliance at entry and exit.

The founders can’t sell, can’t move, can’t borrow, can’t yield. Satoshi (Bitcoin) holds $100 billion and cannot spend a dollar of it. Buterin (Ethereum) sells $6.6 million and triggers a market crisis. CZ (Binance) sits on $65 billion in functionally frozen assets. Adams (Uniswap) cannot execute a treasury grant without a governance revolt. The Arbitrum Foundation watches its token bleed to near-zero while its chain hits all-time highs. Armstrong (Coinbase) — the one founder who straddles both worlds — demonstrates through his TradFi stock sales exactly what infrastructure makes possible: orderly, compliant, market-neutral liquidity access.

And within ten years, every dormant holder — Satoshi included — will be forced to move anyway because quantum computing will make dormancy lethal.

When that forced migration happens, every holder who doesn’t have a privacy layer will be deanonymized, front-run, and exposed. The ones who survive with their wealth and security intact will be the ones who migrated through compliant privacy infrastructure before the quantum deadline hit.

Soulbound Finance is building that infrastructure. KYC at deposit. Privacy at transaction. Yield on assets. Compliance by design. Tax settlement at off-ramp, in your jurisdiction, through established channels.

The Equities Gap between TradFi wealth management and crypto is the largest unsolved problem in digital assets. Every cycle produces another public demonstration of what happens without the right tools — another foundation excoriated for funding operations, another founder selling into a down market because no alternative exists, another team watching their token bleed to zero while their product hits all-time highs, while across the aisle, their TradFi counterparts execute identical transactions through private, compliant mechanisms and the market doesn’t blink.

Soulbound closes the gap.

References

Lookonchain. “vitalik.eth is dumping $ETH fast — 2,961.5 ETH ($6.6M) sold at average price of $2,228.” On-chain analytics, February 5, 2026.

https://x.com/lookonchain/status/1887050637012799944

SEC Form 4 — Brian Armstrong / Coinbase Global (NASDAQ: COIN). Armstrong sold 449,155 shares (~$163M) via Rule 10b5-1 plan, June 25-26, 2025. One of eight disclosed sales totaling hundreds of millions since November 2024. Zero market disruption. https://www.stocktitan.net/sec-filings/COIN/form-4-coinbase-global-inc-insider-trading-activity-840a41106005.html

Wikipedia — Changpeng Zhao. Forbes estimates CZ’s net worth at $88 billion (October 2025). Holds ~90% of Binance, ~89M BNB tokens (98% of portfolio). Presidential pardon granted October 23, 2025. https://en.wikipedia.org/wiki/Changpeng_Zhao

Crypto Briefing. “Uniswap Grantees Slammed for Dumping $10M in UNI.” DeFi Education Fund sold half its allocation in a single OTC transaction. Curve Finance’s Charlie Watkins cited “opaque lobbying organisations.” July 2021. https://cryptobriefing.com/uniswap-grantees-slammed-dumping-10m-uni/

Bybit — Arbitrum (ARB) Price Data. All-time high: $2.39 (January 12, 2024). All-time low: $0.1245 (February 4, 2026). Decline exceeding 94% while Arbitrum chain metrics posted all-time highs. https://www.bybit.com/en/price/arbitrum/

Alpha Research Group is a blockchain and AI venture incubator focused on infrastructure-layer investments. Soulbound Finance provides privacy-preserving payment infrastructure and wealth management for digital asset holders.

Disclaimer: This article discusses financial strategies for informational purposes only and does not constitute financial, legal, or tax advice. Consult qualified professionals for guidance specific to your situation. Alpha Research Group has a financial interest in Soulbound Finance.

| A guest post by

|