From Robot to Android: The $7 Trillion Feature

A Hidden Signal for Humanoid Robotics’ Domestic Inflection Point

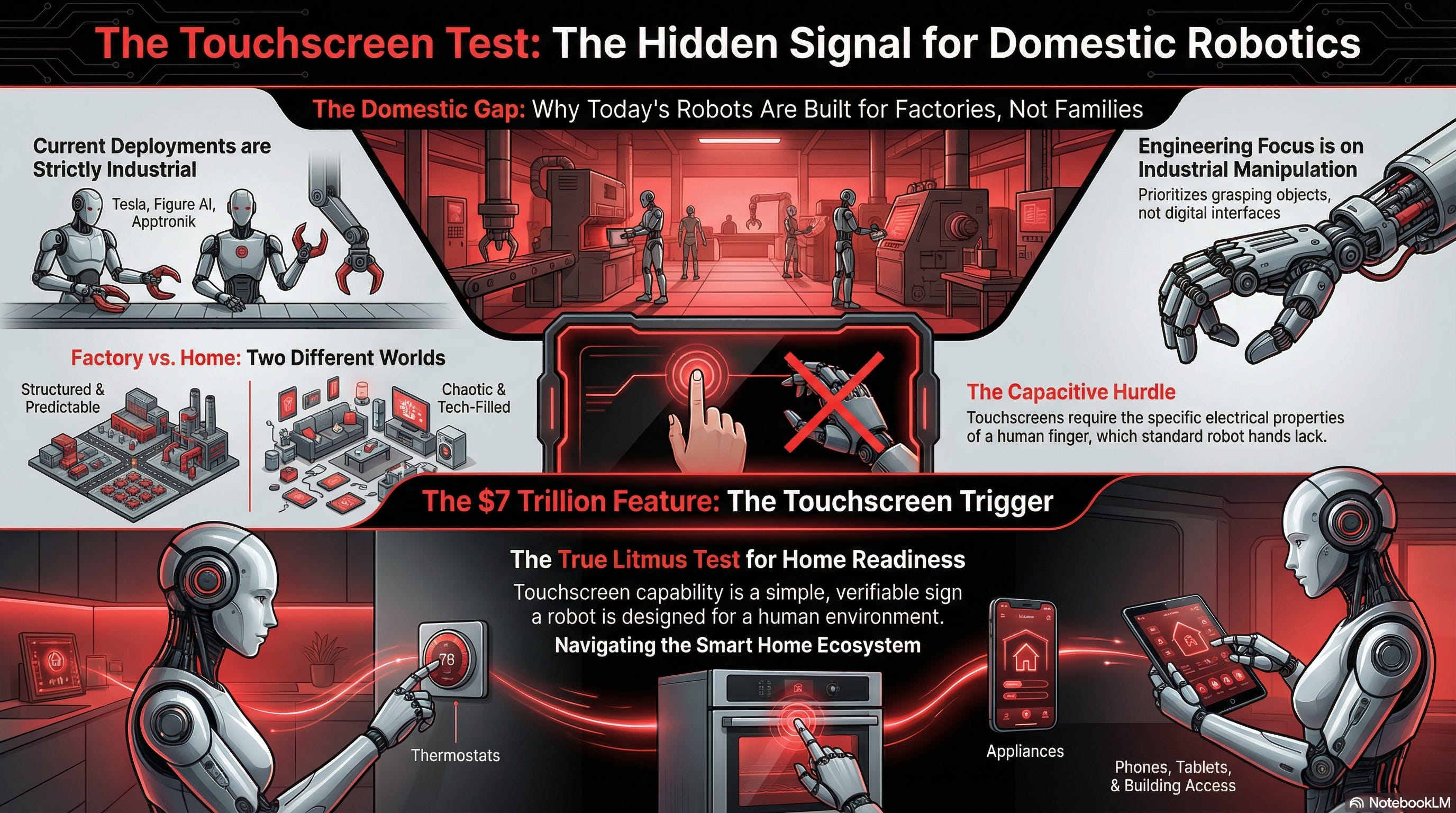

The humanoid robotics industry is currently drowning in hype, inflated production targets, and demo videos that range from impressive to outright fraudulent. Separating signal from noise requires identifying metrics that cut through the marketing theater. We propose one such metric: capacitive touchscreen compatibility.

When a humanoid robot can reliably operate a standard smartphone or tablet touchscreen, the industry will have crossed a threshold from industrial prototype to genuine domestic deployment readiness. This seemingly mundane capability serves as a proxy for the entire constellation of engineering decisions required to make a robot that actually lives alongside humans rather than merely performing in controlled warehouse environments.

The Current State: Industrial Focus, Domestic Fantasy

The humanoid robotics market is experiencing unprecedented capital inflow and production scaling. Tesla has announced targets of 10,000 Optimus units in 2025, scaling to 100,000 monthly by 2026. Chinese manufacturer Unitree shocked the market in July 2025 by launching the R1 humanoid at $5,900—a price point previously thought impossible. Figure AI plans to scale its Figure 03 production to 100,000 units annually by 2029. Global robotics investment in 2025 has already exceeded 20 billion yuan, with more than 82% of deals taking place in China.

Yet virtually all current deployments remain industrial:

Agility Robotics’ Digit operates in Amazon fulfillment centers and GXO logistics facilities

Apptronik’s Apollo handles bin tasks in Mercedes-Benz European plants

UBTECH’s Walker S1 trains in BYD and Dongfeng automotive factories

Tesla’s Optimus is deployed internally for battery production line tasks

The gap between these controlled warehouse environments and the chaos of a typical home remains vast. Factories offer structured layouts, predictable lighting, standardized equipment, and minimal interaction with fragile humans. Homes present the opposite: variable surfaces, pets, children, stairs, miscellaneous clutter, and critically—a universe of consumer electronics designed exclusively for human fingers.

Why Capacitive Touch Matters

Modern capacitive touchscreens operate by detecting changes in electrical charge when a conductive object (a human finger) approaches the screen surface. The screen creates an electrostatic field, and the finger’s body capacitance disrupts this field in a measurable way. This is why standard styluses, gloves, and most prosthetic fingers fail to register.

For a robot to operate a touchscreen, it must either:

Replicate human finger electrical properties: Match the dielectric characteristics and grounding properties of human tissue

Generate its own capacitive signature: Use internal circuitry to simulate the charge disruption pattern

Bypass capacitance entirely: Use alternate sensing modalities that don’t interact with existing consumer devices

The prosthetics industry has largely solved this problem. Companies like Motorica use graphene nanotube-infused conductive silicone fingertips that transmit electrical currents from the residual limb. More sophisticated bionic hands use internal electronic circuits to generate the required capacitive signal. These solutions exist, work reliably, and cost relatively little to implement.

Yet no major humanoid robotics manufacturer has prioritized this capability. The reason is simple: they don’t need it for their current use cases.

The Engineering Priorities Tell the Story

Tesla has devoted approximately half of its Optimus engineering resources to hand development. The Optimus Gen 3 hand features 22 degrees of freedom—approaching the human hand’s 27 degrees—with tendon-driven actuation, tactile sensors, and increasingly sophisticated grasping capabilities. This represents genuine advancement.

But the focus is on manipulation for industrial tasks: picking objects, placing components, handling materials. The hands are designed to interact with the physical world of factories, not the digital interfaces of homes.

Similarly, Figure AI’s fourth-generation mechanical hands emphasize torque, precision, and durability. Unitree’s hand development prioritizes AI algorithm integration for learning-based manipulation. Across the industry, hand development addresses the question: “How do we grasp and move objects?” rather than “How do we interact with the devices humans already use?”

This prioritization makes economic sense. Industrial deployments generate revenue. Warehouse automation has clear ROI calculations. A robot that can move 1,000 boxes per shift creates measurable value. A robot that can adjust your thermostat touchscreen creates... convenience.

The Domestic Deployment Trigger

The inflection point arrives when manufacturers genuinely commit to domestic deployment. 1X Technologies has taken the first step with NEO, available for pre-order at $20,000 with deliveries beginning in 2026. Figure AI has announced alpha testing in homes beginning in 2025. LG will debut CLOiD at CES 2026, explicitly targeting household tasks.

When these robots actually enter homes, capacitive touch becomes table stakes. Consider the interfaces a domestic robot must navigate:

Smartphones and tablets for receiving instructions and providing feedback

Smart home control panels for thermostats, lighting, security systems

Appliance touchscreens on modern refrigerators, ovens, washing machines

Elevator and building access panels in multi-unit housing

Kiosks and payment terminals for errands and assisted living scenarios

A domestic robot that cannot operate these interfaces is fundamentally limited. It cannot adjust the thermostat when instructed. It cannot start the dishwasher after loading it. It cannot interact with the ecosystem of consumer electronics that define modern home environments.

The workaround—API integration with smart home platforms—only partially addresses this. Many devices lack API access. Legacy equipment has no connected capabilities. And the value proposition of a “general purpose” humanoid collapses if it requires custom integration for every device it might encounter.

The Bellwether Feature

We propose tracking capacitive touchscreen compatibility as a binary indicator of domestic deployment seriousness. This metric has several advantages:

Simplicity: Either the robot can operate a standard smartphone, or it cannot. No ambiguous definitions or arguable interpretations.

Non-headline status: No manufacturer will prematurely announce this capability for marketing purposes. It’s too mundane to generate excitement, too easy to verify, and too obviously irrelevant to current industrial applications.

Proxy for integration thinking: Solving capacitive touch requires considering how the robot’s materials, electrical systems, and grounding interact with existing consumer devices. This represents a shift from “robot as isolated system” to “robot as participant in human environment.”

Technical feasibility: The prosthetics industry has solved this problem multiple times. The engineering is well-understood. Absence of implementation reflects prioritization, not capability.

Competitive Landscape

United States

Tesla Optimus: Focus remains on industrial deployment. Hand development prioritizes dexterity for manipulation tasks. No announced work on capacitive compatibility. Commercial sales targeted for 2026, but domestic applications remain downstream of factory deployment.

Figure AI: Most aggressive domestic timeline with alpha home testing in 2025. Best positioned to prioritize interface compatibility as home trials reveal real-world limitations. Figure 03 features advanced manipulation but no confirmed capacitive capability.

Agility Robotics: Digit remains warehouse-focused. No domestic timeline announced. Unlikely early adopter of capacitive touch.

Apptronik Apollo: Industrial trajectory with Mercedes-Benz partnership. No domestic pivot indicated.

China

Unitree Robotics: Aggressive pricing strategy ($5,900 R1) suggests consumer market ambitions. CEO Wang Xingxing predicts industry “iPhone moment” within 3-5 years. Price competitiveness could accelerate domestic adoption pressure.

UBTECH: Walker S series in automotive factory trials. Strong government backing but industrial focus dominates.

Agibot (Zhiyuan Robotics): Service-oriented positioning with A2 targeting customer engagement. Closer to domestic use cases but current focus on commercial rather than residential.

Galaxy Universal Robotics: Raised 1.3 billion yuan within two years. Well-funded for rapid development but deployment focus remains unclear.

Europe/Other

1X Technologies (Norway): NEO explicitly designed for household use. $20,000 price point with 2026 delivery. Most directly committed to domestic deployment. Prime candidate to implement capacitive touch as home trials reveal interface limitations.

LG CLOiD: CES 2026 debut targeting household tasks. Consumer electronics heritage positions LG to understand interface ecosystem requirements.

Conclusion

The humanoid robotics industry is racing toward production scale without clear consensus on what “domestic deployment” actually requires. Current development priorities reflect industrial revenue opportunities rather than home environment realities.

Capacitive touchscreen compatibility serves as a useful, verifiable, non-gameable indicator of when manufacturers cross from industrial focus to genuine domestic commitment. The capability is technically solved, economically trivial, and strategically revealing.

When humanoid robots can use your iPhone, they’re ready to live in your house. Until then, they’re warehouse equipment with better marketing.

Alpha Research Group maintains detailed timeline projections, component supplier analysis, and investment frameworks for the humanoid robotics sector. For access to our full research including adoption curves and positioning recommendations, contact us at info@alpharesearchgroup.com.

| A guest post by

|